This guest post is by Wilfred Brockmann, our Chief Investment Officer. I want to tell you something that might sound counterintuitive: The moment you feel most compelled to do something with your portfolio is usually the exact moment you should do nothing at all.

Knowledge without implementation is worthless. Understanding why systematic approaches work is only valuable if you can actually follow them consistently.

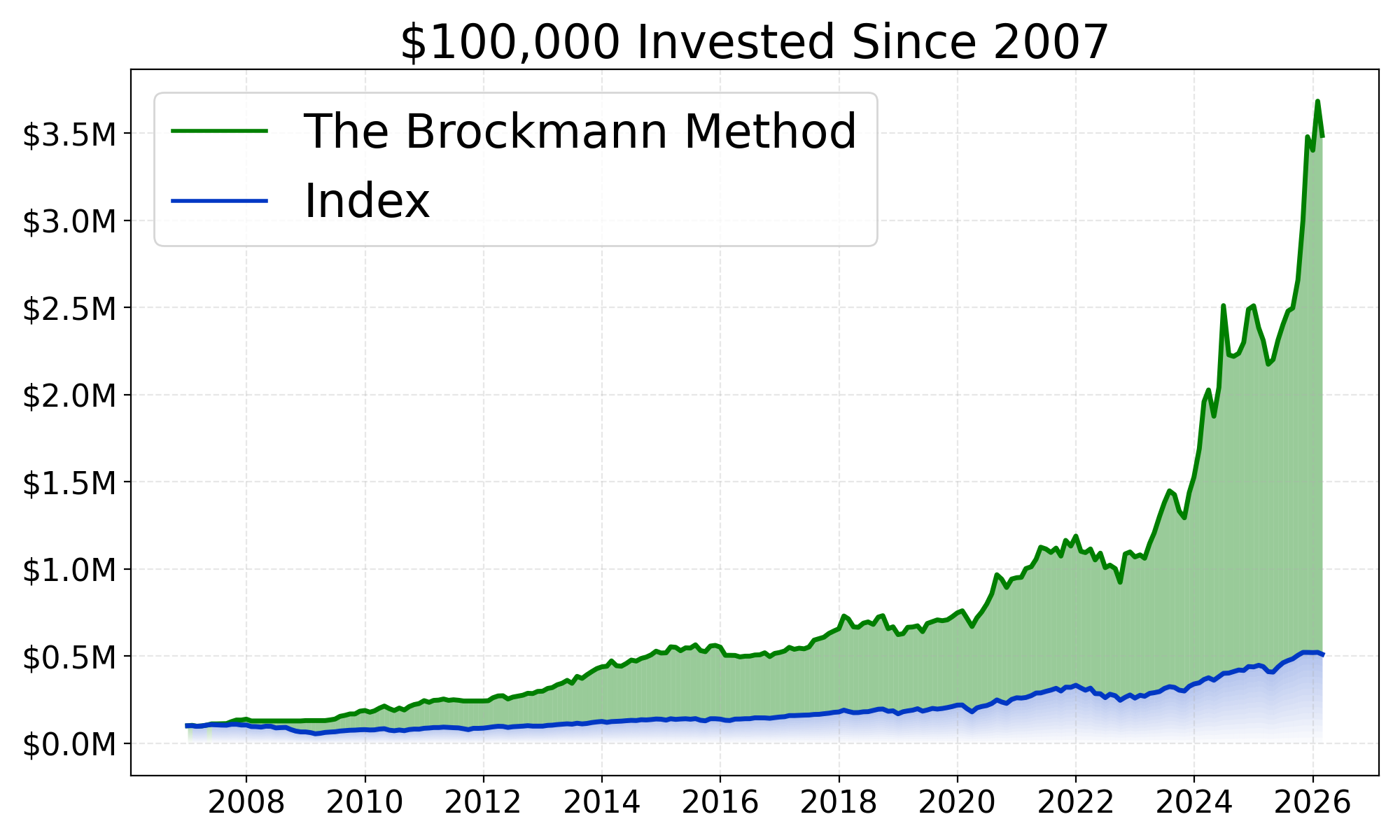

Building investment discipline requires more than good intentions—it requires process.

Numbers don't lie. While investment philosophies and market theories can be debated endlessly, mathematical evidence provides objective insights into what actually works.

The data consistently supports systematic approaches over discretionary investing.

The average investor consistently underperforms the market. According to Dalbar's Quantitative Analysis of Investor Behavior, the average equity investor returned 7.13% annually over the past 20 years while the S&P 500 returned 10.5%.

Financial media creates the illusion that investing success comes from having the latest information. Turn on any business channel and you'll see urgent market updates, breaking news alerts, and expert opinions delivered with the authority of fact.

Every year, millions of investors try to pick winning stocks. They research companies, analyze earnings reports, follow analyst recommendations, and make careful selections for their portfolios.

Most of them lose to the market.

We’re excited to announce the release of BeyondETFs Pro v5.1.0, now available for download on the App Store and Google Play. This update builds on the foundation of version 5 and brings powerful enhancements, smarter insights, and a more intuitive experience for self-directed investors like you.

Last week, we stuck to our process. As always, we ran our rankings at the regular time in the regular way. No drama, no deviation. Then, a few hours later, the world shook—Israel attacked Iran’s nuclear infrastructure. Headlines screamed. Markets looked jumpy. And I did what many might do: I picked up the phone and called Wilf.

🔄 The market moves every day — and so do we

At BeyondETFs, we update our rankings every single day. That’s right — every day, we evaluate all 100 stocks in the S&P 100 and recalculate their standing in the Brockmann Method.

Great news!

Stability improvements. Faster and more reliable functions. New 'Chat with the Founders' feature. Creating an account as a Basic or Pro subscribers generates an entirely new chat experience, where subscribers can text the founders, Wilf and Peter Brockmann for suggestions, to answer questions, product support or just to say hi (something our non-founder brother does).